A report from the U.S. Government Accountability Office (GAO) finds that most borrowers in income-dependent repayment (IDR) plans have low income. The report also finds that borrowers in these repayment plans are less likely to be in default. This demonstrates that the repayment plans are functioning as intended, as a safety net for borrowers facing financial difficulty.

The report, Federal Student Loans: Education Could Do More to Help Ensure Borrowers Are Aware of Repayment and Forgiveness Options (GAO-15-663) was published on August 25, 2015 and publicly released on September 17, 2015.

A Small Percentage of Eligible Borrowers Participate in IDR

As of September 2014, about one-fifth (19%) of borrowers in the Direct Loan program are in income-dependent repayment plans, with 4% in Income-Contingent Repayment (ICR), 13% in Income-Based Repayment (IBR) and 2% in Pay-As-You-Earn Repayment (PAYE).

In September 2012, the U.S. Department of the Treasury estimated that about half (51%) of borrowers in the Direct Loan program are potentially eligible for IBR. Of eligible borrowers, approximately 20% were participating in ICR or IBR. (PAYE wasn’t available until later in 2012.)

Borrowers Persist in IDR

Most borrowers remain in income-dependent repayment plans, although about 1 in 6 no longer has a partial financial hardship. 95% of borrowers in IBR remain in the repayment plan 2 years later, with 84% still having a reduced payment as compared with standard 10-year repayment. 98% of borrowers in PAYER remain in the plan 1 year later, with 86% still having a reduced payment as compared with standard repayment.

Most Borrowers in IDR are Low-Income

Most borrowers in income-dependent repayment plans are low-income. 70% of borrowers in IBR and 83% of borrowers in PAYE have non-zero annual earnings of $20,000 or less and 10% of borrowers in IBR and 5% of borrowers in PAYE have annual earnings greater than $40,000.

For comparison, 150% of the poverty line is $17,655 for a family size of 1, $23,895 for a family size of 2, $30,135 for a family size of 3 and $36,375 for a family size of 4.

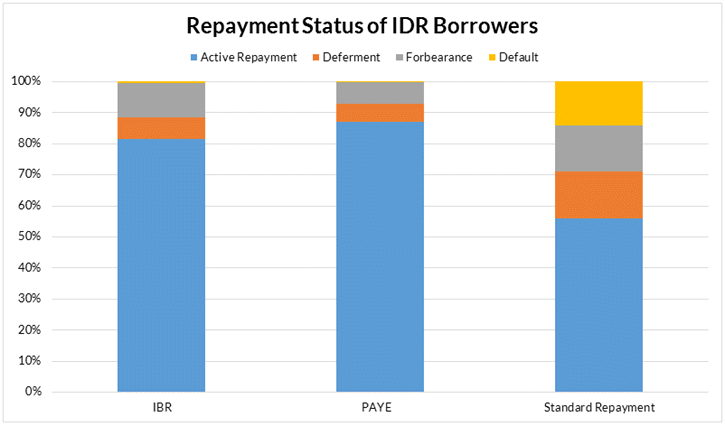

IDR Plans have Reduced Default, Deferment and Forbearance Rates

Income-dependent repayment plans appear to have shifted borrowers away from deferment, forbearance and default, as intended.

- Less than 1% of borrowers in IBR (0.5%) and PAYE (0.1%) have defaulted on their student loans, compared with 14% of borrowers in standard repayment

- 81% of borrowers in IBR and 87% of borrowers in PAYE are in active repayment, compared with 56% of borrowers in standard repayment

- 7% of borrowers in IBR and 6% of borrowers in PAYE are in deferment, compared with 15% of borrowers in standard repayment

- 11% of borrowers in IBR and 7% of borrowers in PAYE are in forbearance, compared with 15% of borrowers in standard repayment

These trends are illustrated by the following chart.

IDR Borrowers May be Unaware of Public Service Loan Forgiveness

An estimated 643,000 Direct Loan borrowers in income-dependent repayment plans are potentially eligible for Public Service Loan Forgiveness (PSLF), but only 147,000 (23%) have had their employment certified as eligible for PSLF. Of borrowers submitting employment certification forms as of September 2014, 72% were approved and 28% were rejected. Reasons for rejection include ineligible loans (14% of applicants), missing or incorrect information on application forms (12%) and ineligible employment (1%).

Average Debt for IDR is Similar to Extended Repayment

The GAO report found that 36% of borrowers in IBR and 55% of borrowers in PAYE had $30,000 or less debt, 22% of borrowers in IBR and 25% of borrowers in PAYE had $30,001 to $50,000 in debt, 26% of borrowers in IBR and 13% of borrowers in PAYE had $50,001 to $100,000 in debt, and only 16% of borrowers in IBR and 7% of borrowers in PAYE had $100,001 or more in debt. The distribution of the number of borrowers by the amount of debt is illustrated by this chart.

Data from the National Student Loan Data System (NSLDS) indicates that the average debt of borrowers in income-dependent repayment plans is above-average. As of June 30, 2015, the average debt was $35,738 for borrowers in ICR, $55,632 for borrowers in IBR and $40,000 for borrowers in PAYE, compared with $16,840 for borrowers in standard repayment and $42,470 for borrowers in extended repayment.