The U.S. Department of Education has released data concerning delinquency rates for federal student loans for the first time. The Department has previously released data concerning total federal loan volume outstanding, loan status and repayment plan.

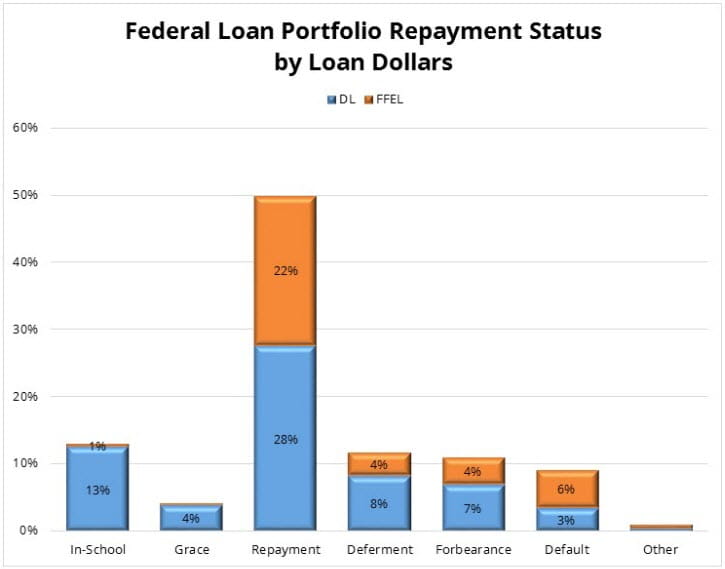

As of June 30, 2014, there was a total of $1.1 trillion of federal education loans outstanding to 39.9 million unduplicated borrowers, representing an increase of $89.7 billion and 1.2 million borrowers over June 30, 2013. About one-third of the dollar loan volume is in the Federal Family Education Loan (FFEL) program and two-thirds in the Federal Direct Loan (DL) program.

Most of the remaining data is available only for loans in the Direct Loan program. The Direct Loan program includes a more recent mix of federal education loans and, therefore, may not be reflective of all federal education loans in repayment. FFEL loans are much more likely to be in repayment than in an in-school or grace period status. Because no new FFEL loans have been made since July 1, 2010, the FFEL loan portfolio is more mature. Most borrowers who default on their student loans do so within 4-5 years of entering repayment. This chart shows the distribution of loan dollars by repayment status.

Of the Direct Loans that are in repayment, deferment or forbearance, 26% of the dollars and 15% of the recipients are in Income-Contingent Repayment (ICR), Income-Based Repayment (IBR) or Pay-as-You-Earn Repayment (PAYER), compared with 38% of the dollars and 61% of the recipients in standard (10-year) repayment.

Delinquency Status

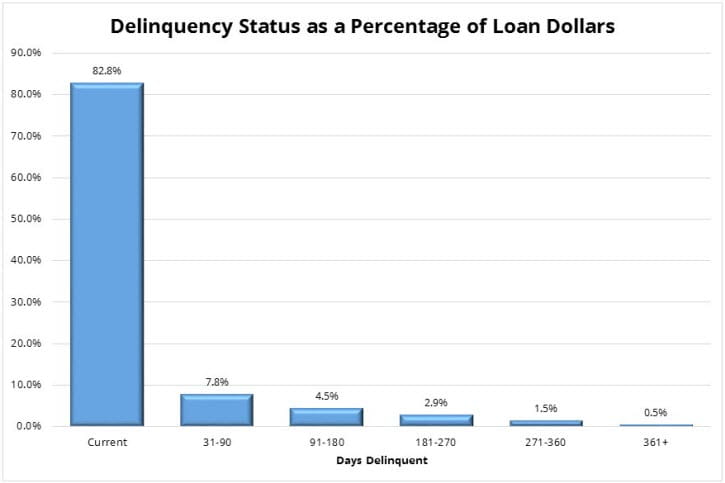

Most of the Direct Loans in repayment are current. As this chart demonstrates, 83% of the dollars are current and 17% are 31 or more days delinquent. More than 9% of the loan dollars are in a serious delinquency, defined as 91 or more days delinquent. Most borrowers who are delinquent will not progress to default, as noted by the Institute for Higher Education Policy (IHEP) in its March 2011 report, Delinquency: The Untold Story of Student Loan Borrowing. Delinquent borrowers often bring the loans current to avoid the negative consequences of default. For example, this chart shows that the percentage of borrowers with a 91-180 day delinquency is smaller than the percentage of borrowers with a 31-90 day delinquency. The percentage of borrowers with a more serious delinquency continues to decline.

Of the Direct Loan dollars that have entered repayment and are not still in an in-school or grace period status, 17.5% are delinquent or in default (12.9% in a serious delinquency or in default), 17.6% are in a deferment and 14.8% are in forbearance. The borrowers in deferment include borrowers who have returned to school for further education, borrowers in a military service deferment and borrowers in an economic hardship deferment.

Interpret Data with Caution

The delinquency and repayment plan data must be interpreted with caution.

- This data involves just loans in the Direct Loan program, omitting loans in the FFEL program. Data concerning delinquency rates based solely on loans in the Direct Loan program may reflect a more recent mix of loans, overstating overall delinquency rates for federal education loans.

- This analysis is based on loan dollars, not borrowers. Although the data includes both dollars outstanding and the number of loan recipients, it is not possible to remove duplicates from calculations involving the number of recipients. This could lead to double-counting of borrowers who have loans in more than one repayment plan or more than one repayment status.

- It is important to distinguish between borrowers who are still in an in-school or grace period status and borrowers who have already entered repayment. Borrowers who are in an in-school or grace period status are not required to make payments on their loans.

- The data does not distinguish between borrowers who are in a deferment because of financial difficulty and borrowers who are in a deferment because they have returned to school or are in a military service deferment. Most of the borrowers in a deferment are in an in-school or military service deferment, not an economic hardship deferment.